Training Day serves as the inaugural day of the annual ECB Simulation Conference for university students, where distinguished representatives from institutions, businesses, and academia share their knowledge and experiences with the participants.

The Training Day for the 9th Conference took place at the Bank of Greece on November 21, 2024.

The key themes of the Conference were:

The 9th Conference was made possible thanks to the invaluable support of the Bank of Greece, the Hellenic Bank Association, Dialectica, Piraeus Bank, Bernitsas Law, and the Athens University of Economics and Business.

Here, we highlight the positions of the speakers of the Training Day of the 9th ECB Simulation Conference. We are greatly honoured to have speakers such as Ms. Charoula Apalagaki, Acting General Manager, Hellenic Bank Association, Maria Luís Albuquerque, Commissioner (2024-2029) | Financial Services and the Savings and Investments Union (via a recorded message), Mr. Gabriel Glöckler, Principal Adviser, Directorate General Communications, European Central Bank, Mr. Christos Hadjiemmanuil, Professor, University of Piraeus, Visiting Professor, London School of Economics & Member of the Monetary Policy Council, Bank of Greece, Mr. Emmanouil Perakis, Associate Professor of European Union Law, National and Kapodistrian University of Athens, Ms. Ifigeneia Skotida, Deputy Director, Economic Analysis & Research Department, Bank of Greece, Mr. Nikos Magginas, Chief Economist, Head of Economic Analysis Department, National Bank of Greece, Mr. Georgios Gatopoulos, Head of International Macroeconomics and Finance Unit, IOBE, Mr. Dimitrios Dimopoulos, Head of ESG, Piraeus Bank, Ms. Maria Nefeli Bernitsa, Partner Bernitsas Law, Mr. Christos Kalandranis, Associate Professor of Corporate Finance, Department of Accounting and Finance, University of West Attica, Mr. Antonis Ballis, Associate Professor in Finance, Director of MSc FinTech, Aston Business School, Aston University and Mr. Dimitris Anastasiou, Assistant Professor, Department of Business Administration, Athens University of Economics and Business.

The opening remarks concluded with a recorded message from Ms. Maria Luís Albuquerque, who underlined Europe’s need for more effective capital markets and a higher level of financial literacy, so that savings can be channeled into investments supporting growth, as well as technological and green transitions.

Ms. Albuquerque stressed that every financial decision involves risk, making personal finance skills essential. She referred to the first European strategy for financial literacy, which seeks to build citizens’ trust in investment products. She stressed that the shift from saving to investing must become accessible and low-cost, as is the case in countries with developed investment ecosystems such as Japan and Canada.

She concluded her speech by emphasizing the need for an effective European capital markets ecosystem capable of supporting businesses across Europe and ensuring a more efficient allocation of capital.

The Training Day opened with a speech by Ms. Haroula Apalagaki, who highlighted the central role of the Hellenic Bank Association, which works closely with the Bank of Greece and contributes to shaping the Greek banking landscape. She emphasized that the Greek banking system now records a historic low in non-performing loans, strong capital adequacy, and robust profitability—factors that place it among the most resilient in the Eurozone.

Ms. Apalagaki focused on the developments that occurred in 2024, a year marked by interest rate cuts, strengthened stability, and significant progress in instant payments, which now dominate transactions.

She continued by underscoring the role of the ECB as the guarantor of monetary stability and a driving force in the green transition of the financial system. In regards the digital euro initiative, she noted that it aims to strengthen Europe’s independence and competitiveness in the payments landscape. Moreover, Ms. Apalagaki stressed the importance of completing the Banking Union and establishing a European Deposit Insurance Scheme.

In closing, she pointed to the Hellenic Bank Association’s role as a bridge between society and the banking sector, aiming at credible public communication and the enhancement of citizens’ financial literacy.

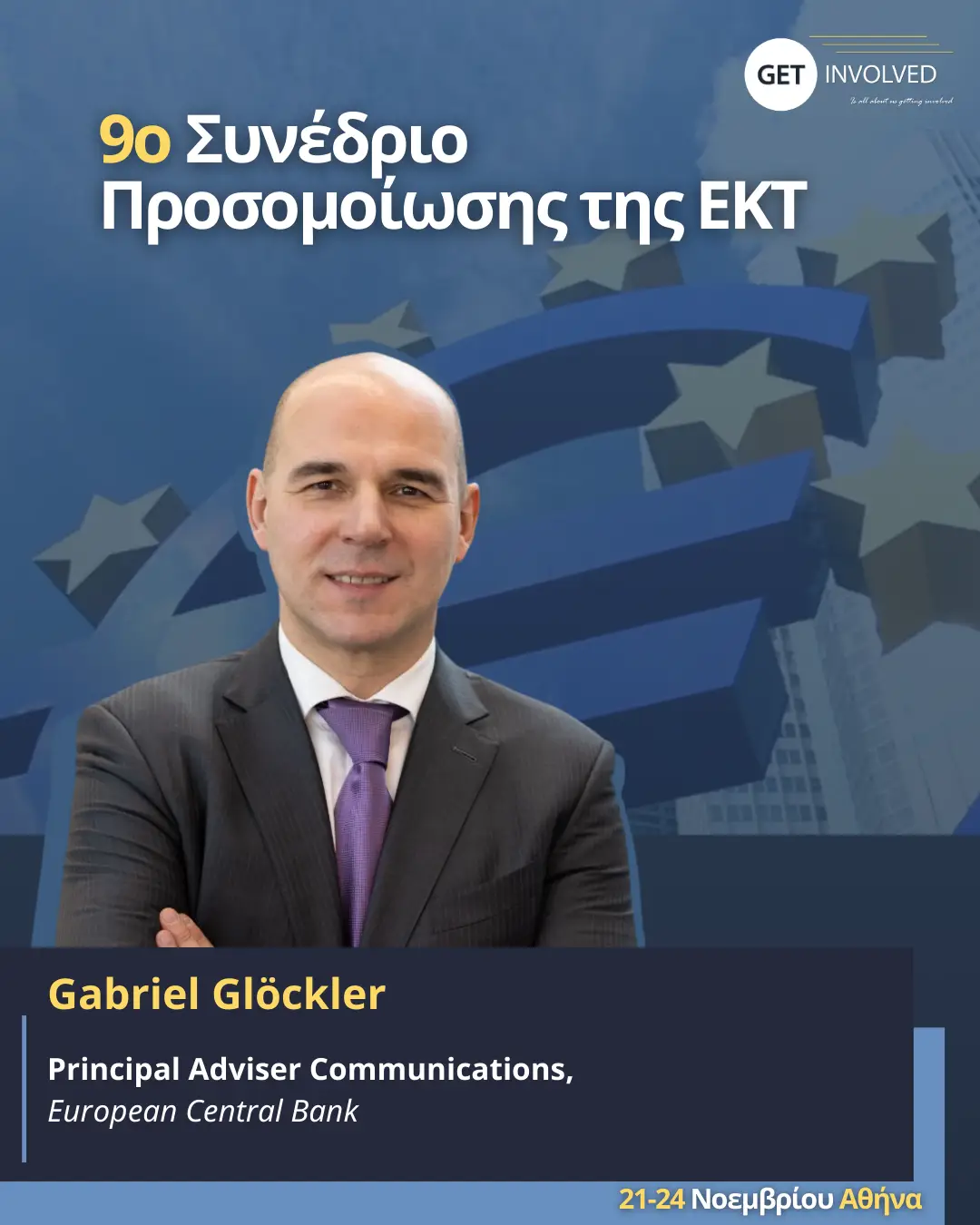

In his address, Mr. Gabriel Glöckler stressed that trust is the ECB’s most important asset and a prerequisite for effective monetary policy. Communication, he stressed, is not an auxiliary tool but an important pillar of policymaking, as the euro rests on shared understanding and acceptance of its value.

Mr. Glöckler highlighted that central banks can no longer rely on communicating using highly technical language; clarity and accessibility are now essential, tailored to different countries, cultures, and levels of financial literacy. The abundance of available—but not always reliable—information makes it necessary to simplify messages without oversimplifying.

Mr. Glöckler noted that the ECB is investing in new forms of communication—short formats, visual explanations, and content for social media—to clarify “what a decision means for the citizen.” Responding to audience questions, he argued that artificial intelligence improves real-time monitoring of developments and helps adapt messages to different audiences, leading to more targeted communication.

The first discussion panel opened with Mr. Christos Hadjiemmanuil, who presented the institutional foundations of the Economic and Monetary Union. He stressed that macroeconomic policy rests on two pillars: monetary and fiscal policy. The initial ambition for full convergence in both areas—traced back to the Werner Report—proved unrealistic, as states would not accept such a loss of sovereignty.

The Maastricht Treaty established a framework in which the ECB enjoys a unique level of independence, constitutionally safeguarded at the Union level. Its mandate remains narrow—price stability—justifying the strict limits on intervention and its high degree of autonomy. However, the sovereign debt crisis exposed functional asymmetries: the ECB is prohibited from financing governments, yet was called upon to act as a guarantor of fiscal stability through various initiatives.

Mr. Hadjiemmanuil concluded by noting that despite progress, coordination between a single monetary policy and national fiscal policies remains imperfect. The Eurozone still operates through intergovernmental cooperation, often burdened by mistrust and divergent national priorities.

Mr. Emmanouil Perakis, continued the discussion by highlighting the financial crisis as a turning point for the Eurozone, revealing the institutional weaknesses of Maastricht. EMU’s architecture had separated monetary from fiscal policy and relied mainly on crisis-prevention mechanisms. When the crisis hit, member states were caught off-guard and had to develop new supranational tools.

This period led to the creation of the European Stability Mechanism (ESM), enhanced surveillance, and the 6-pack and 2-pack reforms—Europe’s first systematic crisis-management tools. The Court of Justice of the EU also played a key role through creative interpretations that allowed the ECB to act at the fringes of its mandate, though these decisions remain debated. With his “whatever it takes” mandate, Mario Draghi turned the ECB into an active defender of economic stability.

Mr. Perakis closed by highlighting the balance between independence and accountability: the ECB’s independence is enshrined in Article 130 TFEU, but it is not unlimited. Accountability is essential for legitimacy, making the proper equilibrium between the two principles indispensable.

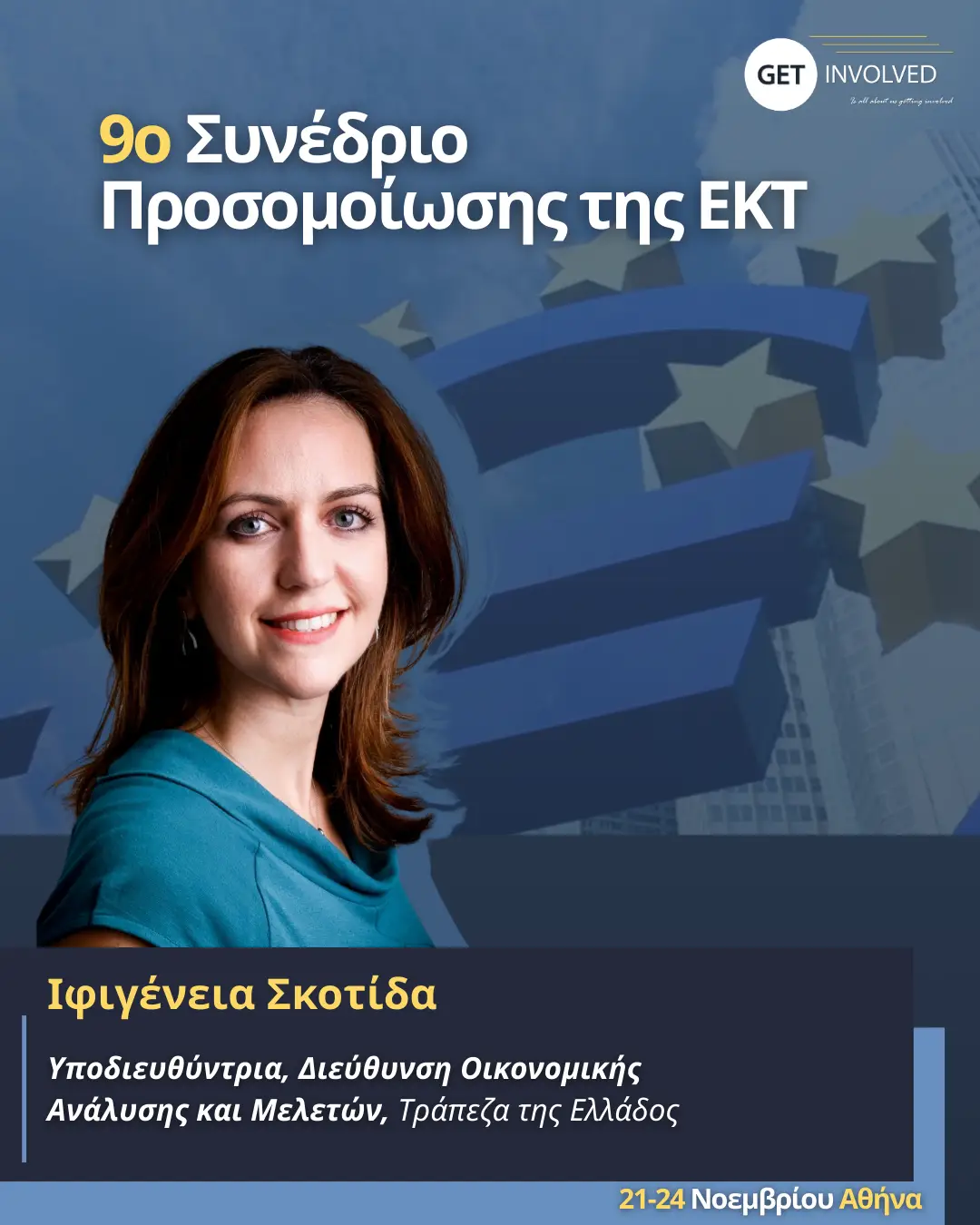

Opening the second panel, Ms. Ifigeneia Skotida presented the ECB’s monetary policy strategy to maintain a symmetric medium-term inflation target of 2%. The medium-term approach allows the ECB to avoid overreacting to short-term inflation shocks while accounting for transmission lags.

The strategy relies on numerous and diverse available tools—policy rates, asset purchase programs, and forward guidance—adjusted to economic conditions. She emphasized the importance of transparency and communication to ensure public and market understanding of ECB decisions.

Following the pandemic and the war in Ukraine, the ECB raised interest rates by a total of 450 basis points to contain inflation without sharply constraining economic activity, aiming for a soft landing. The decline of inflation to 2.5% by mid-2024 confirms the effectiveness of the monetary policy, with forecasts indicating that inflation returns to target in the coming years. ECB lowered interest rates to less restrictive levels, where they remain to this day.

She concluded by noting that uncertainty persists due to geopolitical tensions, tariffs, and demographic challenges.

Closing the panel, Mr. Georgios Gatopoulos presented current trends in the international and Greek economy. He stressed that 2025 is marked by heightened uncertainty, a new wave of U.S. protectionism, and slowing growth in Europe. The global economy is shifting to a new equilibrium characterized by higher tariffs and increased public debt.

He noted that Europe lags in productivity, with the average European producing output roughly 30% lower than the average American. The continent also faces structural challenges: an aging population, defense needs, and an investment gap. Yet, the Eurozone periphery performs better than the core, with Greece steadily reducing public debt and expanding its export orientation.

For Greece, he emphasized that the economy is gradually converging with Europe, driven by export growth, though the investment ratio remains comparatively low. Greece must boost productivity, maintain openness, and safeguard macroeconomic stability.

Mr. Gatopoulos concluded by stating that Europe stands at a critical crossroads and must prioritize effectively while leveraging private capital through partnerships, as fragmented capital markets increase financing costs.

Continuing the speeches, Mr. Nikolaos Magginas highlighted the crucial role of the ECB and central banks in responding to the disruptions of the last decade. He argued that the ECB reacted fastest, using tools such as quantitative easing—an innovation that provided liquidity and stabilized markets, especially for Greece.

He explained that before the crisis, the global economy benefited from low production costs, stable energy prices, and restructured supply chains, creating a prolonged period of stability that allowed monetary policy to operate almost on “autopilot.” Recent crises, however, triggered supply shocks, supply-chain disruptions, and a shift from goods to services inflation, with uneven effects across income groups.

Today, he noted, keeping long-term inflation expectations anchored near 2% is essential for effective transmission, reinforcing the ECB’s credibility. He closed by highlighting emerging challenges: climate change, the green transition, artificial intelligence, and the increasing complexity of tracking productivity- and price-related variables.

Ms. Maria-Nefeli Bernitsa provided a concise overview of the European and national sustainability framework, highlighting the lack of legal literacy as a major barrier. She outlined the evolution of ESG over the last 20 years—from the introduction of the term, to the Paris Agreement, to the EU Taxonomy, the first real attempt to define what constitutes a “sustainable activity”. Together with SFDR and CSRD, these frameworks create unified transparency standards. In Greece, the 2022 Climate Law introduced obligations such as requiring one-third of corporate vehicles to be zero-emission by 2026.

She noted that for many companies, compliance still feels like “box-ticking” due to the volume of obligations and time pressure. Nonetheless, market demand is real—especially for green loans—and banks differ significantly in their level of preparedness.

She also pointed to supervisory challenges: the need for complete and reliable data, detecting greenwashing risks, and the debate around potentially expanding the role of independent authorities. The system, she noted, is self-correcting, but meaningful compliance will strengthen only when sanctions are effectively enforced.

Opening the third discussion panel, Mr. Dimitrios Dimopoulos stressed that sustainability in the banking sector—and beyond—is not optional but a matter of survival. European legislation is evolving in response to rising climate risks, imposing transparency and disclosure rules that increasingly affect even companies without formal compliance obligations.

He noted that a company’s value is no longer defined solely by its financial results. ESG criteria are now essential risk-assessment tools, indicating how well-structured, healthy, and resilient a firm is. Initiatives such as the Network for Greening the Financial System (NGFS) guide banks in managing environmental and climate risks.

Mr. Dimopoulos discussed greenhushing, where companies implement sustainability actions but avoid communicating them due to uncertainty or fear of criticism. He noted that the transition requires societal engagement and that policies must be implemented at a pace allowing smooth adjustment.

He closed by emphasizing that social welfare is the ultimate objective; competitiveness and profitability are necessary but not sufficient for a fair, effective transition.

Mr. Antonis Ballis presented the digital euro as an unavoidable development for a Eurozone that must compete with the digital currencies of other countries and with large international payment platforms. He emphasized that its purpose is not to be “innovative or trendy,” but universally accepted and publicly guaranteed—just like cash.

He noted that the critical question is who will hold the transaction ledger—the ECB or private intermediaries. This decision has major implications for banking stability, as large-scale transfers to the ECB could reduce bank liquidity and constrain profitability.

Mr. Ballis explained that the digital euro is also necessary due to the growing influence of private payment systems that reinforce foreign currencies, such as the U.S. dollar. It also serves as a crisis-management tool, ensuring uninterrupted transactions even if underlying infrastructures fail.

He concluded that implementing the digital euro is above all a political issue, given the EU’s complex multi-stakeholder and multi-state structure.

Mr. Christos Kallandranis opened the final discussion panel by presenting the digital euro as an inevitable step for the Eurozone, noting that the ECB has the adaptability framework needed to implement it. He described it as a “one-way road”, since if Europe does not develop its own digital currency, it will need to adopt an alternative solution.

The digital euro does not reinvent money; it modernizes monetary infrastructure and meets younger generations’ expectations for instant, secure, fully digital payments. Its innovative aspect lies in its institutional design, built on: state guarantee, institutional trust, universal accessibility, and interoperability across the Eurozone.

He explained that the digital euro provides public protection and continuity, unlike private solutions that involve higher risks and dependence on global platforms. He concluded by stressing that it does not compete with the banking system but strengthens competition and improves payment services.

The panel concluded with Mr. Dimitris Anastasiou, who described the digital euro as public money in digital form, fully guaranteed by the ECB. He compared it to a “public PayPal,” available at all times—even during a blackout—offering the highest level of security and reliability.

Its necessity, he noted, is primarily geopolitical, as the Eurozone is heavily dependent on non-European payment platforms and lacks its own infrastructure. The digital euro strengthens Europe’s monetary sovereignty and provides a foundation for innovative private-sector services.

Mr. Anastasiou emphasized that the digital euro does not compete with commercial banks. Strict deposit thresholds will limit how much can be transferred to a Digital Euro Wallet, preserving financial stability. The digital euro’s true competitors are stablecoins and non-European payment platforms.

I am one of the co-founders of Get Involved with which I have participated in the planning and implementation of numerous initiatives that have impacted more than 3,000 university students and graduates. My role entails the coordination of the overall organization, the project management of our various and diverse initiatives, and the strategy formulation.

My work in Get Involved reflects my commitment to have an active role in empowering the youth, their “voices” and to strive to nurture a positive culture where young people can develop to their full potential.

My name is Chrisanthi Indouna, and I am an undergraduate student in the Department of Management Science and Technology at the Athens University of Economics and Business. I joined Get Involved as a Junior Associate in September 2025. I am part of the Operations team, where I contribute, among other tasks, to the organization and coordination of the team’s initiatives. In May 2025, I attended the event “Sustainable Future IV: Beyond Green – Navigating the Future of Sustainability & Innovation”. I acquired valuable insights into sustainable development and its role in contemporary entrepreneurship.

My decision to join Get Involved was driven by my strong interest in youth initiatives and the team’s culture, which encourages creativity, collaboration, and active participation in innovative projects.

For me, Get Involved represents a unique opportunity to expand my knowledge in sustainability and finance. Its youthful spirit and the collaboration among people from different academic backgrounds, united by a shared vision, motivate me to actively engage in projects that have a meaningful impact.

I’m a Law student and since May 2025, I’ve been part of the Communications team at Get Involved. I’ve always been an outgoing person who enjoys working with others, so I immediately felt that this role suits me well. I’m really interested in sustainability, mainly because I feel like we’re the first generation truly experiencing the consequences of the environmental crisis. I believe that each of us can contribute to something better, in our own way. Through this team, I hope to learn, grow, and collaborate with people who share the same concerns and vision. I also hope to bring my own perspective and energy to everything we do.

My name is Konstantina Katsimicha, and I am an undergraduate student at the Department of Economics of the Athens University of Economics and Business.

In 2024, I participated in the 8th ECB Conference; an experience that significantly deepened my understanding of monetary policy, financial institutions, and the broader economic framework of the Εuro area.

In 2025, I joined Get Involved as a Junior Associate in both the Communications and Social Media Management teams. Through this role, I contribute to the promotion of our initiatives and help manage our online presence, while also developing valuable communication, organizational, and teamwork skills.

What inspired me to become part of Get Involved is the team’s vision and spirit to enhance economic literacy among young people and foster a space where ideas, knowledge, and skills can grow through collaboration. Being surrounded by passionate peers committed to impactful initiatives motivates me to learn, evolve, and contribute actively.

My name is Angelina Arfani, and I am an undergraduate student in the Department of Political Science and International Relations at the University of the Peloponnese. I have joined the Get Involved team as a Junior Associate in the Operations and Communications departments, where I contribute to the efficient coordination of initiatives and assist in enhancing the organization’s outreach and engagement.

I believe that Get Involved is an innovative initiative driven by individuals committed to creating meaningful change. Being part of this team has provided me with the opportunity to expand my knowledge, develop key skills, and showcase my abilities, all while collaborating with passionate individuals who share a common vision.

My name is Konstantina Triantafyllopoulou, and I am an undergraduate Political Science & Public Administration university student at the National and Kapodistrian University of Athens. Also, I am currently enrolled in the American College of Greece, pursuing a minor in Human Resources Management.

I joined Get Involved in 2025 as a Junior Associate in the communications team, where I help by communicating with external partners and with the promotion of our initiatives. The key factors that motivated me to join were my ambition to engage within the community and broaden both my understanding and skills around finances, communication, entrepreneurship, and youth-led projects.

Being an active member of Get Involved highlights my keen enthusiasm for promoting financial literacy, actively engaging with the youth community, and embracing the core values of this team.

My name is Lila Kartali and I am an undergraduate student in the Department of International and European Studies at the University of Piraeus. I joined the team in February 2024, and since then I have happily been part of the Corporate Communications, Social Media, External Opportunities, and Scientific team. The diversity of the topics I deal with in each department, as well as the collaboration and interaction with ambitious people, are a pleasant challenge for me.

For me, Get Involved is an opportunity to develop various skills and strengthen my knowledge background on sustainability and monetary policy issues. Moreover, the fact that it is a youth initiative, by people from different scientific fields collaborating for a common goal, is the reason why I want to be part of it.

As an active member of Get Involved’s Associates, I am part of engaging and continuously evolving projects centered on strengthening financial literacy among young people in Greece and Europe. Moreover, by combining my studies in computer science, I am an integral part of Get Involved’s ongoing digital transformation journey.

My contributions to Get Involved reflect my commitment to supporting its ultimate goal of social contribution and raising awareness of financial literacy issues among youth.

My name is Maria Anastasopoulou and I am an undergraduate student at the Law School of the National and Kapodistrian University of Athens. My participation in Get Involved started in 2023, whereas now I am an Associate and a member of the Legal Team, where I help handle the group’s legal issues, prepare legal educational materials and represent the group in the ECB Simulation Conference. Additionally, I participate in the stream for Student and Youth Organizations, where I develop my communication skills by interacting with external partners and other youth initiatives. I am also a member of the Scientific Team and contribute to the structuring of the group’s studies, such as the “ESG & Sustainability Youth Perspectives”, while simultaneously developing my research and writing skills.

The drive behind my involvement with the team is the exceptional academic and research level of my colleagues and the passion for the field. The shared values of mutual respect, the desire for progress and innovation, and continuous new’ goal setting, motivate me to contribute and join in a common evolutionary path.

I am particularly grateful for my participation in Get Involved, as it provides me the opportunity to significantly broaden my economic and legal knowledge, delve further into areas of interest and collaborate with some of the most active and accomplished young people, from whom I learn daily.

Apostolos Karasakalidis holds a bachelor’s degree in law (2023) from Aristotle University of Thessaloniki, a master’s degree in European Business and Economic Law (2025) from the same university, and is currently pursuing an advanced master’s program in Intellectual Property and Information and Communication Technologies (ICT) Law at KU Leuven. He is a certified Data Protection Officer (DPO) and is registered with the Thessaloniki Bar Association as a lawyer.

He has been a Legal Associate at Get Involved since August 2022 and became Scientific Associate in April 2025. Apostolos participates in Get Involved because he believes in the added value of collaboration among young scholars from different academic backgrounds. Furthermore, he is interested in the green transition of the EU economy and supports the promotion of financial literacy among young people.

“Opportunities don’t just come to you – Υou create them.” – Chris Grosser

I joined Get Involved in 2019, I have progressed to the role of Senior Associate, and I currently am a member of the Legal Team. My participation in the team has provided me with valuable opportunities, and experiences, and it has given me the chance to work with numerous active youths. I have taken part in various initiatives, such as the ECB Simulation Conferences, and have had multiple responsibilities, including developing educational materials and participating in the communications team. I appreciate Get Involved’s commitment to fostering a collaborative environment that empowers young university students and professionals.

Thanasis Dogramatzidis is an executive in the Financial Assets Management department at the Central Bank of Malta. Previously, he worked as a trader at the National Bank of Greece.

He holds an MSc in International and European Governance and Politics from the National and Kapodistrian University of Athens an MSc in Finance and Banking, and a BSc in Statistics, both from the Athens University of Economics and Business.

In 2024, Thanasis became a Scientific Associate at Get Involved, driven by his belief in the need to advance economic literacy and highlight contemporary economic issues, especially within the realm of monetary policy.

Antonis Ballis holds a Doctoral degree in Finance (2021) from Athens University of Economics and Business, a specialized Master’s degree in Applied Economics and Data Analysis (2016) from the University of Patras (2016), and a Bachelor’s degree in Economics (2014) from Athens University of Economics and Business. In 2018 he was awarded full funding for his doctoral research on cryptocurrencies, from the Greek State Scholarships Foundation (IKY). His main research areas are Cryptocurrency/DEFI Economics, Behavioral Finance, and Financial Technology (FinTech).

“Success consists of going from failure to failure without loss of enthusiasm.” – Winston Churchill